Inflation #1

While the subject of inflation is always a hot topic in financial markets, I expect it will be even more so over the coming years as we start to see the potential effects of the experiments being conducted by central banks around the world. When I find interesting commentary relating to inflation, I’ll add it to a post in a running series on the topic.

For this first post, I’ve included commentary from two very different investors. The first excerpt is from John Hussman and his May 2020 Market Comment, which I thought provided a great summary of the macro causes of inflation. The second excerpt contains comments by Warren Buffett from the 1980s—when he seemed especially worried about inflation—on the types of businesses likely to do well in an inflationary environment.

Predicting inflation is hard, and predicting its timing is probably close to impossible. But if it arrives, it will have a major influence on asset prices. And predicting which assets are better suited to do well in such an environment is a more achievable undertaking.

As Mr. Buffett wrote in his 2008 Annual Letter, about and during the financial crisis:

This debilitating spiral has spurred our government to take massive action. In poker terms, the Treasury and the Fed have gone “all in.” Economic medicine that was previously meted out by the cupful has recently been dispensed by the barrel. These once-unthinkable dosages will almost certainly bring on unwelcome aftereffects. Their precise nature is anyone’s guess, though one likely consequence is an onslaught of inflation. Moreover, major industries have become dependent on Federal assistance, and they will be followed by cities and states bearing mind-boggling requests. Weaning these entities from the public teat will be a political challenge. They won’t leave willingly.

Those comments are even more relevant today in the wake of the crisis caused by COVID-19, and the government response to it.

John Hussman’s May 2020 comments on inflation:

I’ve often emphasized that just like these pieces of paper we call “stocks,” these pieces of paper we call money have an enormous psychological component to their pricing. In fact, if you spend a great deal of time with data, you’ll discover that the effort to model inflation as a stable function of money supply, output, unemployment, and other variables is among the most comical wastes of time you’ll ever undertake.

Much of my thinking on inflation is captured in my August 2019 comment, How To Needlessly Produce Inflation. What follows largely mirrors that discussion.

If you study substantial inflations, you’ll find that they typically emerged in the context of large government deficits coupled with supply shocks. Consider Germany in 1929. As France and Belgium invaded the German industrial area in the Ruhr, protesting workers went on a mass strike, and the German government decided to pay them anyway, despite the fact that their production had dropped sharply. This combination of events should ring bells. It certainly has in the U.S. gold market in recent months.

Government deficits are funded by creating pieces of paper – namely government bonds, or if the central bank buys those bonds, base money. If the public believes that the government has a credible ability to retire its liabilities, or at least keep them from growing at a rate that’s not too different from the growth rate of the real economy, then people may be entirely content to hold those pieces of paper without being revolted by doing so.

As long as the public has confidence in government liabilities, the Fed can do as much “quantitative easing” as it wants – buying government bonds and replacing them with base money – or vice versa, and it won’t change the underlying belief that those pieces of government paper are “good” – regardless of which form they take.

Quantitative easing doesn’t directly produce inflation, and whatever inflation we get will not be the result of QE. The policy may have an indirect effect on inflation by encouraging Congress to run larger deficits than it otherwise might. In any event, what inflation requires is public revulsion to government liabilities, and what produces public revulsion is the creation of government liabilities at a rate that destabilizes the expectation that those liabilities remain sound.

As economist Peter Bernholz has noted: “There has never occurred a hyperinflation in history which was not caused by a huge budget deficit of the state… In all cases of hyperinflation deficits amounting to more than 20 per cent of public expenditures are present.”

Moreover, even the size of the deficit has to be placed in context. See, deficits regularly expand during recessions, and tend to contract during economic expansions. The public is sufficiently familiar with this tendency that large deficits during economic downturns rarely cause inflation pressure. Rather, I would assert that revulsion generally kicks in when deficits become what I’d call “cyclically excessive” – that is, persistently larger than one would expect, given the current point in the economic cycle.

Put simply, quantitative easing merely changes the mix of securities that the public holds. That in itself doesn’t create inflation. Historically, inflation has been provoked by government deficits that create new government liabilities at a “cyclically excessive” and unsustainable pace. Conversely, episodes of runaway inflation have regularly been ended by restoring public faith that fiscal and monetary policy have returned to a sustainable course.

So it’s not simply currency creation that creates inflation, but currency creation for the purpose of financing government deficits to such an extent that public confidence in government liabilities is destabilized. The inflationary consequences tend to be particularly severe when these deficits occur during “supply shocks” when production of goods and services becomes constrained for one reason or another.

In his analysis of major hyperinflations, Nobel economist Thomas Sargent (also my former dissertation advisor at Stanford) observed:

“In each case we have studied, once it became widely understood that the government would not rely on the central bank for its finances, the inflation terminated and the exchanges stabilized. We have further seen that it was not simply the increasing quantity of central bank notes that caused the hyperinflation, since in each case the note circulation continued to grow rapidly after the exchange rate and price level had been stabilized. Rather, it was the growth of fiat currency which was unbacked, or backed only by government bills, which there never was a prospect to retire through taxation.”

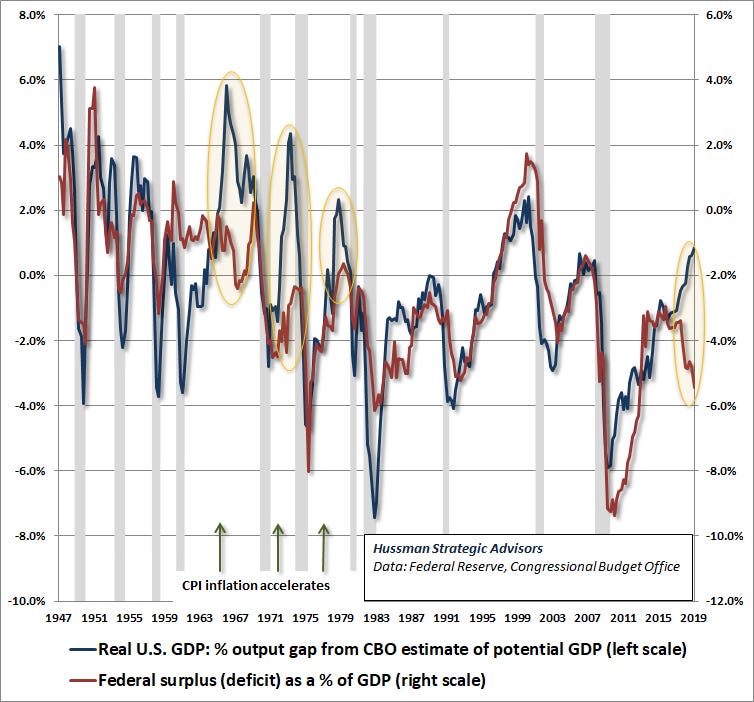

The chart below is from my August 2019 market comment, and shows the U.S. real GDP output gap (the difference between actual real GDP and potential real GDP, based on Congressional Budget Office estimates), along with the U.S. federal surplus or deficit, as a percentage of GDP. Notice that the two generally move together, reflecting a tendency toward smaller deficits or even surpluses during periods of economic strength, and larger deficits during periods of economic weakness.

Notice that there are a few periods when the U.S. economy was operating near full capacity (blue line near or above zero on the left scale), yet government deficits were significant and even expanding (red line well below zero on the right scale). These differences are circled in yellow. The notable feature of all of the prior instances is that they were exactly the points when the inflation rates accelerated. Even in 2019, the government deficit spending was already significantly out-of-line with the position of the U.S. economy.

Again, if the public believes that the government has a credible ability to retire its liabilities, or at least keep them from growing at a rate that’s not too different from the growth rate of the real economy, then people may be entirely content to hold those pieces of paper without being revolted by doing so.

Despite Milton Friedman’s dictum, inflation is not simply a monetary phenomenon. It is a fiscal one. When fiscal deficits become extreme, excessive money creation usually follows. But at its core, inflation reflects revulsion to holding government liabilities. It doesn’t actually matter whether these liabilities take the form of bonds or currency, because revulsion to those liabilities is enough to systematically devalue both of them.

Will inflation bail out a hypervalued stock market? Don’t bet on it. As I detailed in my February market comment, Whatever They’re Doing, It’s Not Investment, the first casualty of inflation is market valuations. With the most reliable measures of market valuation presently about 2.5 times their historical norms, the CPI would have to more than double before the beneficial effects of inflation on nominal growth would outweigh the negative effects of inflation on market valuations. Until that happens, higher inflation will only make matters worse for investors.

The fact is that cash – short-term interest-bearing liquidity – has clearly outperformed the stock market during periods of rising inflation. Indeed, when the rate of inflation is rising, higher rates of inflation are typically associated with poorer stock market performance until market valuations are driven to historically depressed levels (after which the effect of inflation on nominal growth finally dominates).

With respect to deflation risk, the largest contributor on that front would be mass bankruptcies coupled with the avoidance of what I call “cyclically excessive” government deficits. In that environment, stocks would be wiped out, but risk-aversion among investors would likely encourage investors to treat cash as a safe haven, increasing the value of dollars relative to real goods and services (which is what we call deflation). That’s essentially what we observed during the Great Depression. We can’t rule out that prospect, but at present, the deficit and monetary spigots appear wide open.

Warren Buffett’s Comments on Inflation:

From Warren Buffett’s 1981 Letter to Shareholders:

In fairness, we should acknowledge that some acquisition records have been dazzling. Two major categories stand out.

The first involves companies that, through design or accident, have purchased only businesses that are particularly well adapted to an inflationary environment. Such favored business must have two characteristics: (1) an ability to increase prices rather easily (even when product demand is flat and capacity is not fully utilized) without fear of significant loss of either market share or unit volume, and (2) an ability to accommodate large dollar volume increases in business (often produced more by inflation than by real growth) with only minor additional investment of capital. Managers of ordinary ability, focusing solely on acquisition possibilities meeting these tests, have achieved excellent results in recent decades. However, very few enterprises possess both characteristics, and competition to buy those that do has now become fierce to the point of being self-defeating.

The second category involves the managerial superstars - men who can recognize that rare prince who is disguised as a toad, and who have managerial abilities that enable them to peel away the disguise. We salute such managers as Ben Heineman at Northwest Industries, Henry Singleton at Teledyne, Erwin Zaban at National Service Industries, and especially Tom Murphy at Capital Cities Communications (a real managerial “twofer”, whose acquisition efforts have been properly focused in Category 1 and whose operating talents also make him a leader of Category 2). From both direct and vicarious experience, we recognize the difficulty and rarity of these executives’ achievements. (So do they; these champs have made very few deals in recent years, and often have found repurchase of their own shares to be the most sensible employment of corporate capital.)

From the Appendix of Warren Buffett’s 1983 Letter to Shareholders:

But what are the economic realities? One reality is that the amortization charges that have been deducted as costs in the earnings statement each year since acquisition of See’s were not true economic costs. We know that because See’s last year earned $13 million after taxes on about $20 million of net tangible assets – a performance indicating the existence of economic Goodwill far larger than the total original cost of our accounting Goodwill. In other words, while accounting Goodwill regularly decreased from the moment of purchase, economic Goodwill increased in irregular but very substantial fashion.

Another reality is that annual amortization charges in the future will not correspond to economic costs. It is possible, of course, that See’s economic Goodwill will disappear. But it won’t shrink in even decrements or anything remotely resembling them. What is more likely is that the Goodwill will increase – in current, if not in constant, dollars – because of inflation.

That probability exists because true economic Goodwill tends to rise in nominal value proportionally with inflation. To illustrate how this works, let’s contrast a See’s kind of business with a more mundane business. When we purchased See’s in 1972, it will be recalled, it was earning about $2 million on $8 million of net tangible assets. Let us assume that our hypothetical mundane business then had $2 million of earnings also, but needed $18 million in net tangible assets for normal operations. Earning only 11% on required tangible assets, that mundane business would possess little or no economic Goodwill.

A business like that, therefore, might well have sold for the value of its net tangible assets, or for $18 million. In contrast, we paid $25 million for See’s, even though it had no more in earnings and less than half as much in "honest-to-God" assets. Could less really have been more, as our purchase price implied? The answer is "yes" – even if both businesses were expected to have flat unit volume – as long as you anticipated, as we did in 1972, a world of continuous inflation.

To understand why, imagine the effect that a doubling of the price level would subsequently have on the two businesses. Both would need to double their nominal earnings to $4 million to keep themselves even with inflation. This would seem to be no great trick: just sell the same number of units at double earlier prices and, assuming profit margins remain unchanged, profits also must double.

But, crucially, to bring that about, both businesses probably would have to double their nominal investment in net tangible assets, since that is the kind of economic requirement that inflation usually imposes on businesses, both good and bad. A doubling of dollar sales means correspondingly more dollars must be employed immediately in receivables and inventories. Dollars employed in fixed assets will respond more slowly to inflation, but probably just as surely. And all of this inflation-required investment will produce no improvement in rate of return. The motivation for this investment is the survival of the business, not the prosperity of the owner.

Remember, however, that See’s had net tangible assets of only $8 million. So it would only have had to commit an additional $8 million to finance the capital needs imposed by inflation. The mundane business, meanwhile, had a burden over twice as large – a need for $18 million of additional capital.

After the dust had settled, the mundane business, now earning $4 million annually, might still be worth the value of its tangible assets, or $36 million. That means its owners would have gained only a dollar of nominal value for every new dollar invested. (This is the same dollar-for-dollar result they would have achieved if they had added money to a savings account.)

See’s, however, also earning $4 million, might be worth $50 million if valued (as it logically would be) on the same basis as it was at the time of our purchase. So it would have gained $25 million in nominal value while the owners were putting up only $8 million in additional capital – over $3 of nominal value gained for each $1 invested.

Remember, even so, that the owners of the See’s kind of business were forced by inflation to ante up $8 million in additional capital just to stay even in real profits. Any unleveraged business that requires some net tangible assets to operate (and almost all do) is hurt by inflation. Businesses needing little in the way of tangible assets simply are hurt the least.

And that fact, of course, has been hard for many people to grasp. For years the traditional wisdom – long on tradition, short on wisdom – held that inflation protection was best provided by businesses laden with natural resources, plants and machinery, or other tangible assets ("In Goods We Trust"). It doesn’t work that way. Asset-heavy businesses generally earn low rates of return – rates that often barely provide enough capital to fund the inflationary needs of the existing business, with nothing left over for real growth, for distribution to owners, or for acquisition of new businesses.

In contrast, a disproportionate number of the great business fortunes built up during the inflationary years arose from ownership of operations that combined intangibles of lasting value with relatively minor requirements for tangible assets. In such cases earnings have bounded upward in nominal dollars, and these dollars have been largely available for the acquisition of additional businesses. This phenomenon has been particularly evident in the communications business. That business has required little in the way of tangible investment – yet its franchises have endured. During inflation, Goodwill is the gift that keeps giving.

But that statement applies, naturally, only to true economic Goodwill. Spurious accounting Goodwill – and there is plenty of it around – is another matter. When an overexcited management purchases a business at a silly price, the same accounting niceties described earlier are observed. Because it can’t go anywhere else, the silliness ends up in the Goodwill account. Considering the lack of managerial discipline that created the account, under such circumstances it might better be labeled "No-Will". Whatever the term, the 40-year ritual typically is observed and the adrenalin so capitalized remains on the books as an "asset" just as if the acquisition had been a sensible one.

From Warren Buffett’s 1984 Letter to Shareholders:

While there is not much to choose between bonds and stocks (as a class) when annual inflation is in the 5%-10% range, runaway inflation is a different story. In that circumstance, a diversified stock portfolio would almost surely suffer an enormous loss in real value. But bonds already outstanding would suffer far more. Thus, we think an all-bond portfolio carries a small but unacceptable “wipe out” risk, and we require any purchase of long-term bonds to clear a special hurdle. Only when bond purchases appear decidedly superior to other business opportunities will we engage in them. Those occasions are likely to be few and far between.